Open RAN – Where Are We?

By: Stefan Pongratz

Five years have passed since AT&T, China Mobile, Deutsche Telekom, NTT DoCoMo, and Orange founded the O-RAN Alliance back in 2018, with the mission to “reshape the Radio Access Network (RAN) industry towards more intelligent, open, virtualized, and fully interoperable mobile networks.” The O-RAN Alliance also envisioned that the O-RAN specifications would ultimately improve supplier diversity, user experience, RAN efficiencies, and operations by the carriers. As we just wrapped up the full-year results for the 2022 RAN market, the timing is right to review the progress—where are we in this journey to reshape the RAN?

First, let’s review some definitions. At a high level, we can conceptualize the RAN architectures aimed at reshaping the RAN with three high-level tracks, including Distributed RAN (D-RAN) to Centralized RAN (C-RAN), Purpose-Built RAN to Virtualized RAN (vRAN), and Proprietary RAN to Open RAN. Cloud RAN is another term used to capture vRAN deployments adhering to cloud-native design principles. While these architectures and industry terms are at times used interchangeably, the reality is that the drivers, benefits, and competitive landscapes are different, especially now in this initial stage. In addition, the expectations and the risks vary significantly, meaning the probability that operators will mix and match the baseband and the radio with 6G is different than the likelihood that the operators will use vRAN with 6G. At the same time, the overlap ratio will evolve over time and most Open RAN will likely also be Open vRAN in the future, but there will also be some vRAN that is not Open RAN.

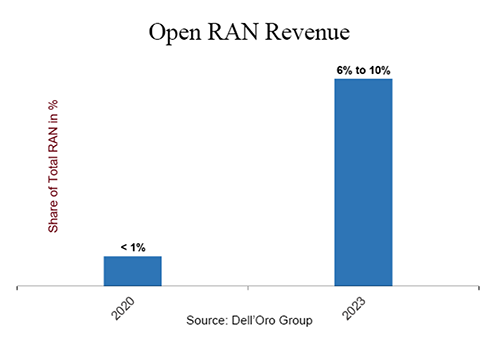

Figure 1: Open RAN Revenue

Figure 1: Open RAN Revenue

For now, we are treating Open RAN and vRAN differently. It is also worth pointing out that when we discuss Open RAN revenues, we measure O-RAN and OpenRAN manufacturer radio and baseband revenues. Similar to other technology transitions, revenue recognition is not always synchronized with operator deployments, especially in the early stages. From a revenue perspective, Open RAN is accelerating (see figure 1 above). Preliminary findings per Dell’Oro’s 4Q22 RAN report suggest Open RAN revenues (O-RAN and OpenRAN radios and baseband) comprised a mid-single-digit share of the overall RAN market in 2022, underpinned by robust greenfield adoption and improving brownfield traction in the US and Japan. The European operators are ahead of the rest of the world when it comes to announcing Open RAN targets; however, they have been more cautious with deploying Open RAN. Instead they are focusing on building out 5G using traditional RAN. As a result, North America and the Asia Pacific regions accounted for more than 95 percent of the 2022 Open RAN