Making Cents with Mobile Money

An additional service is mobile financial services management, essentially online banking. This is typically delivered through a mobile app by a financial institution, and banks are indeed the leading players in this space, in terms of both app uptake/usage and investment dollars. However, open APIs are enabling a new class of services, such as those offered by MINT, that converge multiple financial accounts into one mobile app.

Finally, there is the movement into becoming an actual financial service provider by partnering with banks and/or credit card companies to effectively white label mobile banking. Service providers such as Telenor, Orange, T-Mobile, and Vodafone have taken this route.

Bad timing for ISIS

The initial operator-driven mobile money platform in the United States has suffered numerous setbacks. Three leading operators--AT&T, Verizon, and T-Mobile--joined forces to create a mobile payment platform called ISIS. After many false starts and a very slow market rollout, the service was nearly derailed by its brand name. In July, 2014, Micahel Abbott, ISIS CEO, explained the issue:

“Recently, we have observed with growing concern a militant group whose name, when translated into English, is Islamic State of Iraq and Syria – often referenced by the acronym ISIS. The ISIS militant group has been linked to sectarian violence against civilians and government forces in Iraq and Syria. However coincidental, we have no interest in sharing a name with a group whose name has become synonymous with violence and our hearts go out to those who are suffering. As a company, we have made the decision to rebrand.”

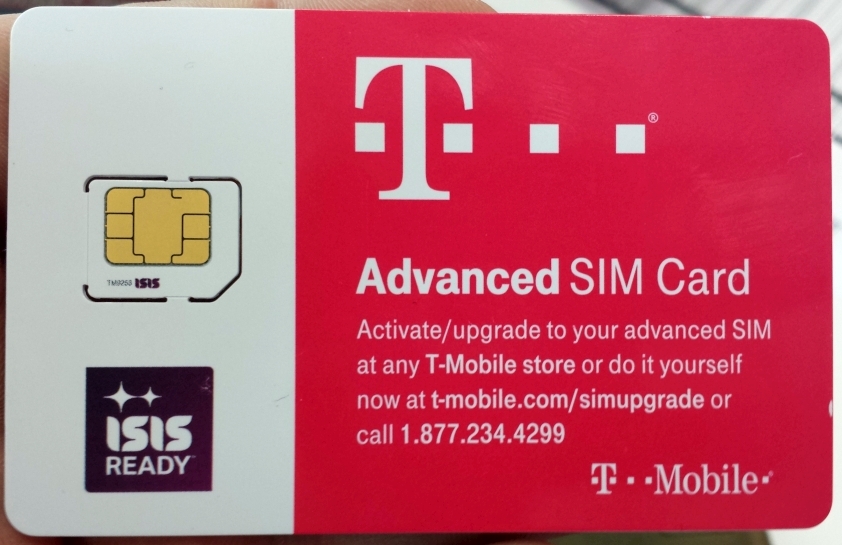

As recently as October of 2014, however, SIM cards from T-Mobile still were branded “ISIS Ready,” and retail stores had ISIS signs on their exterior.

Since then, the service has rebranded as SoftCard. It attempts to assuage security concerns, SoftCard offers features like PIN lock, remote device lock, a dedicated “secure chip” environment, and a unique transaction ID that the group says makes counterfeiting more difficult. However, SoftCard has a lot of work to do in terms of ease of use and convenience, as only a limited number of payment methods can be attached to the SoftCard account.

A similar strategy developed by operators in the UK was abandoned in 2014. Vodafone, EE, and O2 created Weve, a multi-operator mobile wallet offering, last year. In September, 2014, roughly six months after announcing the initiative, the companies scrapped the project.

Fig. 1: ISIS-based SIM cards, still in circulation at the end of 2014

Partnering with banks is a win-win

One of the reasons mobile payments haven’t caught on in the developed world is because current financial services are either too complex, time consuming or expensive for small, daily transactions. Mobile commerce enables banks and operators to mobilize this “long tail” of small transactions by making payments simpler, more affordable and easily accessible for the whole value chain. When banks and operators come together, they can turn these small revenue streams into big business by using mobility as a means to offer every consumer the benefits of being a banking customer: convenience, security, inclusion and empowerment.

Like telecommunications itself, the mobile money opportunity depends on overcoming one of the greatest hurdles for adoption today: ensuring interoperability. It doesn’t matter how many mobile or financial services a consumer can choose from if these services are unable to talk to each other.